Recent Blog Post

What Are the Capital Gains Rules When Selling a Home in San Jose?

Recent Blog Post

What are the capital gains rules when selling a home in San Jose?

Most San Jose homeowners qualify for the federal exclusion that shields $250,000–$500,000 of profit from taxes. Your tax outcome depends on factors such as ownership, residency, and whether the property was your primary home.

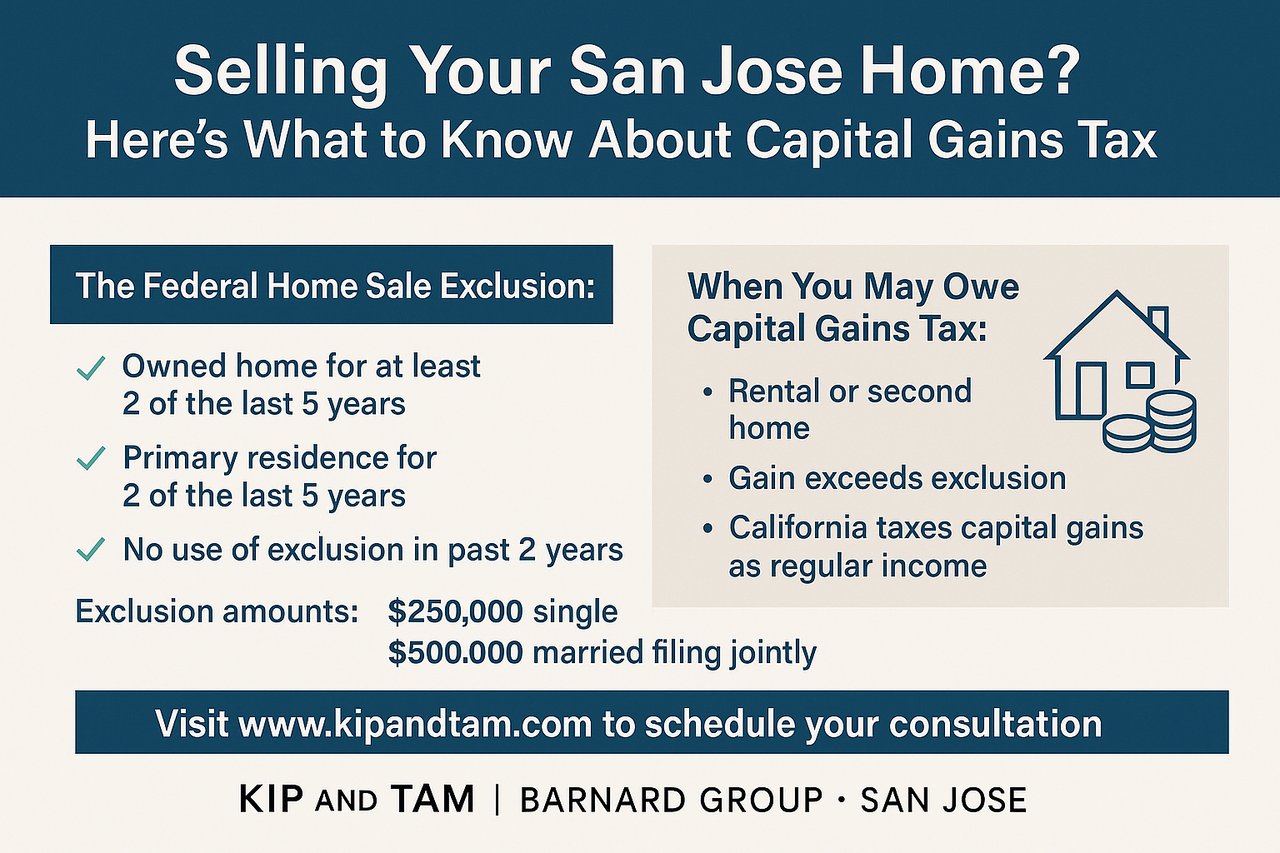

Capital gains tax applies when you sell a property for more than your adjusted cost basis. However, federal law allows many primary‑residence sellers in San Jose to avoid paying taxes entirely.

You can exclude capital gains if:

- You lived in the home for at least **2 of the last 5 years** (residency test)

- You owned the home for at least **2 of the last 5 years** (ownership test)

- You haven’t used the exclusion in the past two years

Exclusion amounts:

- **$250,000** for individuals

- **$500,000** for married couples filing jointly

You may owe tax if:

- Your property is a rental or second home

- Your gain exceeds the exclusion

- You haven’t lived in the home long enough

- You used the exclusion recently

California taxes capital gains as **regular income**, meaning high‑income sellers may owe an additional 9–13% even if federal rules exclude part of the gain. A CPA can provide an exact number.

Your taxable gain is based on the difference between your sale price and your **adjusted cost basis**. You may be able to include:

- Major improvements (kitchen remodels, additions)

- Certain closing costs from the purchase

- Selling costs such as commissions and escrow fees

You bought your San Jose home for $950,000 and sell for $1.7M. After selling costs, your gain might be ~$650,000. If married and eligible for the $500,000 exclusion, you may owe tax only on the remaining $150,000.

Investment properties do not qualify for the exclusion, but a **1031 Exchange** can defer taxes if you purchase another investment property. This has strict deadlines and rules—consult a tax advisor or 1031 intermediary.

Kip and Tam of The Barnard Group at Compass help sellers understand potential tax implications, gather improvement records, and collaborate with your CPA early so there are no surprises when you sell.

Thinking about selling your San Jose home? Kip and Tam can help you understand the tax rules and connect you with trusted local tax professionals.

Visit www.kipandtam.com to schedule your consultation.

Disclaimer: This article is for general informational purposes only and is not intended as legal, tax, or financial advice. Consult qualified professionals for guidance specific to your situation.

Community

Eight outdoor concert series, one map, zero excuses to stay home this summer

Seller Tips

San Jose

How momentum, pricing, and presentation shape early results.

Seller Tips

What homeowners worry about most before they list.

Buyer Resources

A smarter way to compete in Cambrian, Willow Glen, and across San Jose.

Buyer Tips

Why ADUs are one of the strongest value-add moves for San Jose homeowners in 2026.

Seller Tips

The 5 Must-Haves: Positioning your home for move-in ready condition, flexible work space, and modern efficiency.

Seller Tips

Sharpen Your Strategy: How to achieve strong results even when buyers are cautious and inventory is rising.

Seller Tips

The Real Cost of Overpricing: Why your list price is costing you momentum and money.

We believe the process of buying or selling your home should be enjoyable as well as rewarding. Our commitment to our clients is to work hard and provide them with a hassle-free, fun experience. We know how to make this stressful time much easier with our professional expertise, marketplace knowledge, high-tech marketing strategies as well as our enthusiastic team spirit.